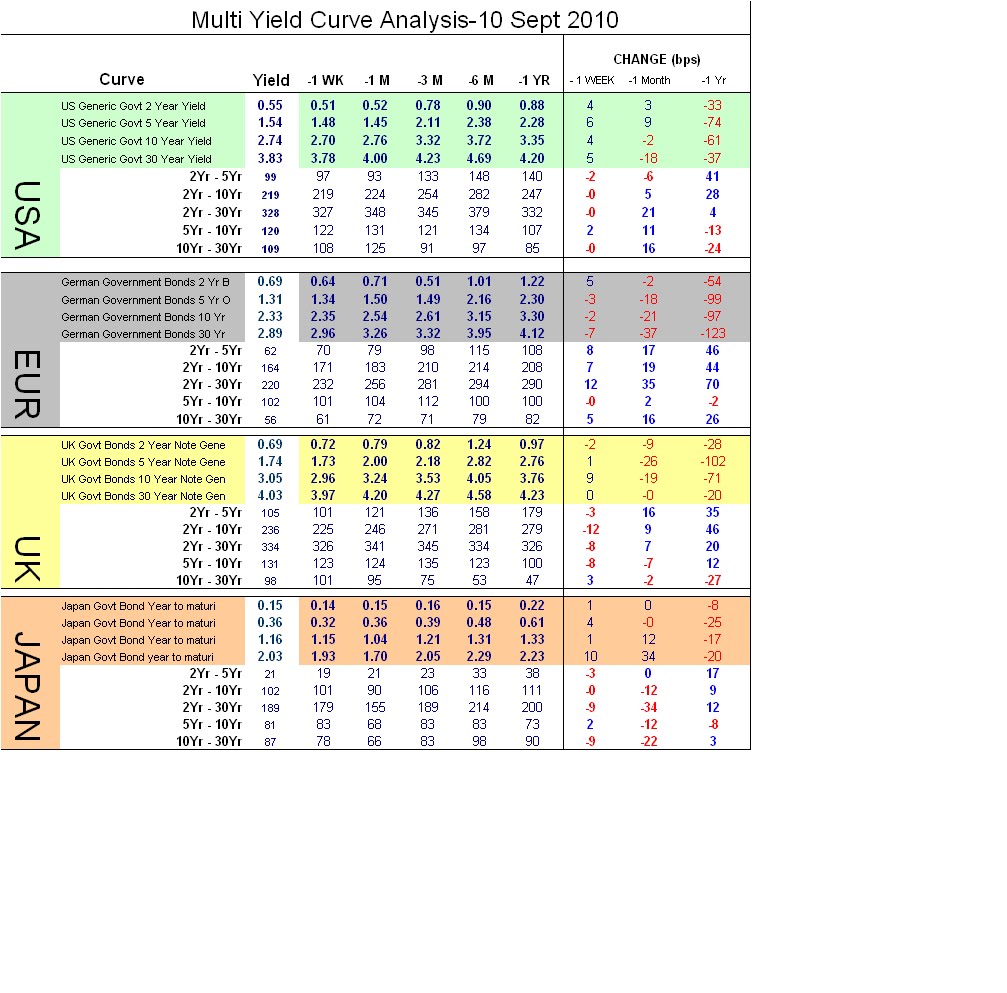

As watchers of this Blog may be already aware, I assign no fundamental economic interpretation to any price movements. I am solely concerned with the Rate of change of prices over various diversified time horizons and what I can predict from statistically analysed results of my Trading models.

We all know, however, that "Momentum" analysis on its own is a lagging indicator and typically on longer term charts often signal at the latter stage of a rally especially following a reversal of a previously persistent trend.

Over the years, I have found it VERY helpful to overlay a particular favourite contrarian indicator of mine namely "Divergence" whether it be up or down.

For the un-initiated, this indicator can identify potential Bull or Bear traps shown when Higher/Lower prices are no longer accompanied with Increasing/Decreasing Momentum.

Of course, Divergence in the Short term can be the catalyst for invaluable market Mean Reversions and an opportunity to re-establish "longs" or "shorts" in the same directiion of the main trend at more advantageous average prices. For example, the DAX could fall 200 pts and yet the Medium momentum trend would still be "UP". So the importance is to attach "Risk" to any particular price by keeping in touch, not just whether momentum is positive or negative, but more imortantly have a measure of the "rate of change" of momentum and predict whether it will continue.

Outlined below, is the latest snapshot of a range of Exchange Traded derivative across the front month contracts in Fixed Interest, Equities. Forex and some Commodities. This of course is only a snapshot and in the real world my models are "adaptive" to real time prices. For an explanation of how these numbers are calculated please refer to earlier posts

Enjoy

Legend

Red - Price statistically Overbought and should experience some Reversion to Mean

Blue - Price statistically Oversold and should experience som Reversion to Mean

Black- Last Price at Posting

Yellow - Central Daily Moving Average Pivot. Close above indicate recent strength. Close below indicates recent weakness

Daily Trend- Positive / Negative / Neutral

St Dev - Rate of change of Daily Trend momentum (Accelerating Up/ Down/ Contracting)